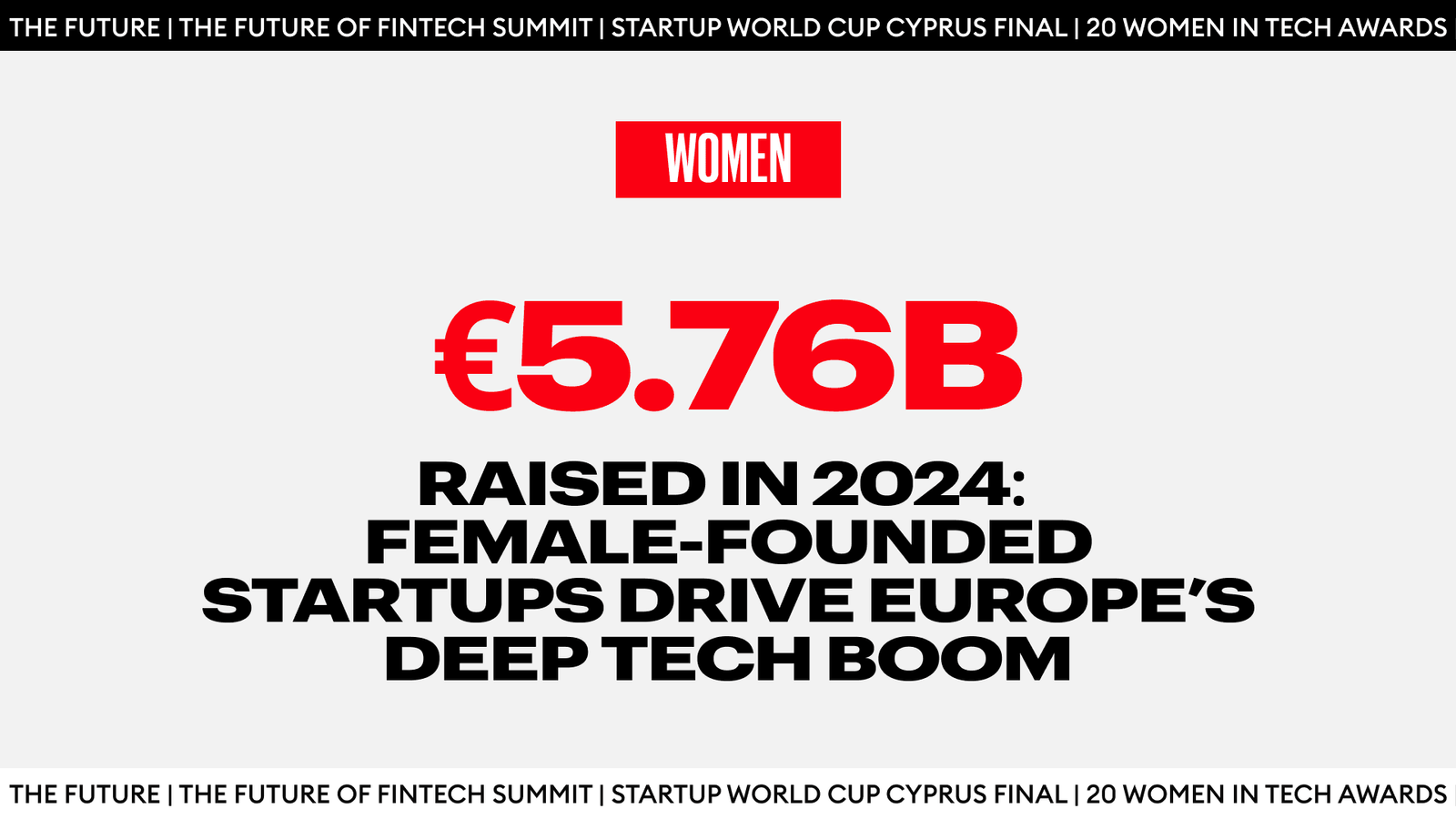

Female entrepreneurs are reshaping Europe’s deep tech sector, securing €5.76 billion in venture capital across 1,305 deals in 2024. Despite a 12% decline from 2023, this aligns with the broader 11% drop in VC funding across all startups, according to the latest Female Foundry and Dealroom report launched at Google HQ in London. The report, Europe’s most comprehensive analysis of female-driven innovation, highlights the growing role of women in scaling high-impact technology ventures.

Investment Trends And Market Shifts

While total funding dipped, female-led startups are demonstrating resilience at key growth stages. Seed-stage companies founded by women are outpacing the broader market, with 20% advancing to Series A compared to 18.9% of all European startups. Smaller funding rounds under $4M have declined by 29%, but larger investments remain stable—$40M-$100M rounds saw only a 1.5% decrease, while $100M-$250M rounds surged by 41.7%.

Follow THE FUTURE on LinkedIn, Facebook, Instagram, X and Telegram

Agata Nowicka, Founder of Female Foundry and lead author of the report, sees this as a pivotal moment. “Innovation is accelerating, and AI is transforming how we live and work. Female founders are seizing opportunities in deep tech to tackle the world’s toughest challenges.”

UK Leads Female-Founded Funding, With Health Tech At the Forefront

Among the top 50 female-founded startups in Europe, standout funding rounds include:

- WorldRemit (€243M)

- The Exploration Company (€150M)

- Newcleo (€135M)

- Pigment (€132M)

- ŌURA (€114.68M)

These companies average 7.6 years in operation, with 81% of their founders having scientific backgrounds. Healthcare dominates at 40%, followed by fintech (14%), food (12%), energy (8%), and transport. The UK leads as the headquarters location for 26% of these startups, followed by France (16%), Germany (10%), Sweden (10%), and Spain (8%).

Women At The Forefront Of Deep Tech’s Growth

Female-led startups secured 33% of all deep tech venture capital in 2024, surpassing the 31% raised by gender-neutral startups. Additionally, 81% of the 50 largest financing rounds in 2024 went to female founders with scientific backgrounds.

In key sectors, funding was led by:

- Synthetic Biology (€282.4M)

- Generative AI (€221.8M)

- Drug Development (€169.9M)

AI is central to this trend; 25% of the top 50 largest female-led funding rounds were in AI-driven startups. Notable raises include Swiss Cradle (€66M), UK-based Dexory (€50M), and Swedish Sana Labs (€50M).

“In the coming years, AI in healthcare, science, and biotech will revolutionize human well-being—curing diseases faster, personalizing treatments, and unlocking scientific breakthroughs,” said Adrian Locher, General Partner at Meantrix.

IPO Momentum And The Path To Unicorn Status

Female-led IPOs are gaining ground. The number of female-founded startups nearing unicorn status rose 40%, from 10 to 14, with the UK, Germany, and France leading this trend. In 2024, three female-led companies hit the $1B mark:

- Newcleo (€135M raised at €1.5B valuation)

- Pigment ($145M at $1B valuation)

- Cardior Pharmaceuticals (acquired by Novo Nordisk for $1B)

The IPO landscape is also evolving, with three successful public offerings: UK-based Raspberry Pi, Bulgaria’s Boleron, and Sweden’s Big Akwa—an increase from just one IPO in 2023.

Challenges And Opportunities For Female Founders

Despite progress, women remain underrepresented in deep tech. Female-led startups account for just 15% of Europe’s deep tech ventures, and all-female teams receive only 2% of total VC funding compared to 5% for mixed-gender teams.

Education gaps and investor biases persist, but targeted support programs—such as equity-free grants and business development initiatives—are helping bridge the divide. Understanding these barriers is key to fostering a more inclusive deep tech ecosystem, ensuring female entrepreneurs continue driving innovation across Europe.