From data center strategy to compliance workflows, geography matters far more in fintech than most pitch decks let on. Even as companies tout their ability to scale anywhere, the reality is that environmental disruption, legal complexity, and infrastructure limitations are often defined by location.

And yet, many fintechs still treat geography as an afterthought, secondary to product-market fit or growth metrics. That oversight carries risk. Geography doesn’t just influence how products are built and deployed; it determines which markets can be entered quickly, which require costly adaptation, and which may never align.

Follow THE FUTURE on LinkedIn, Facebook, Instagram, X and Telegram

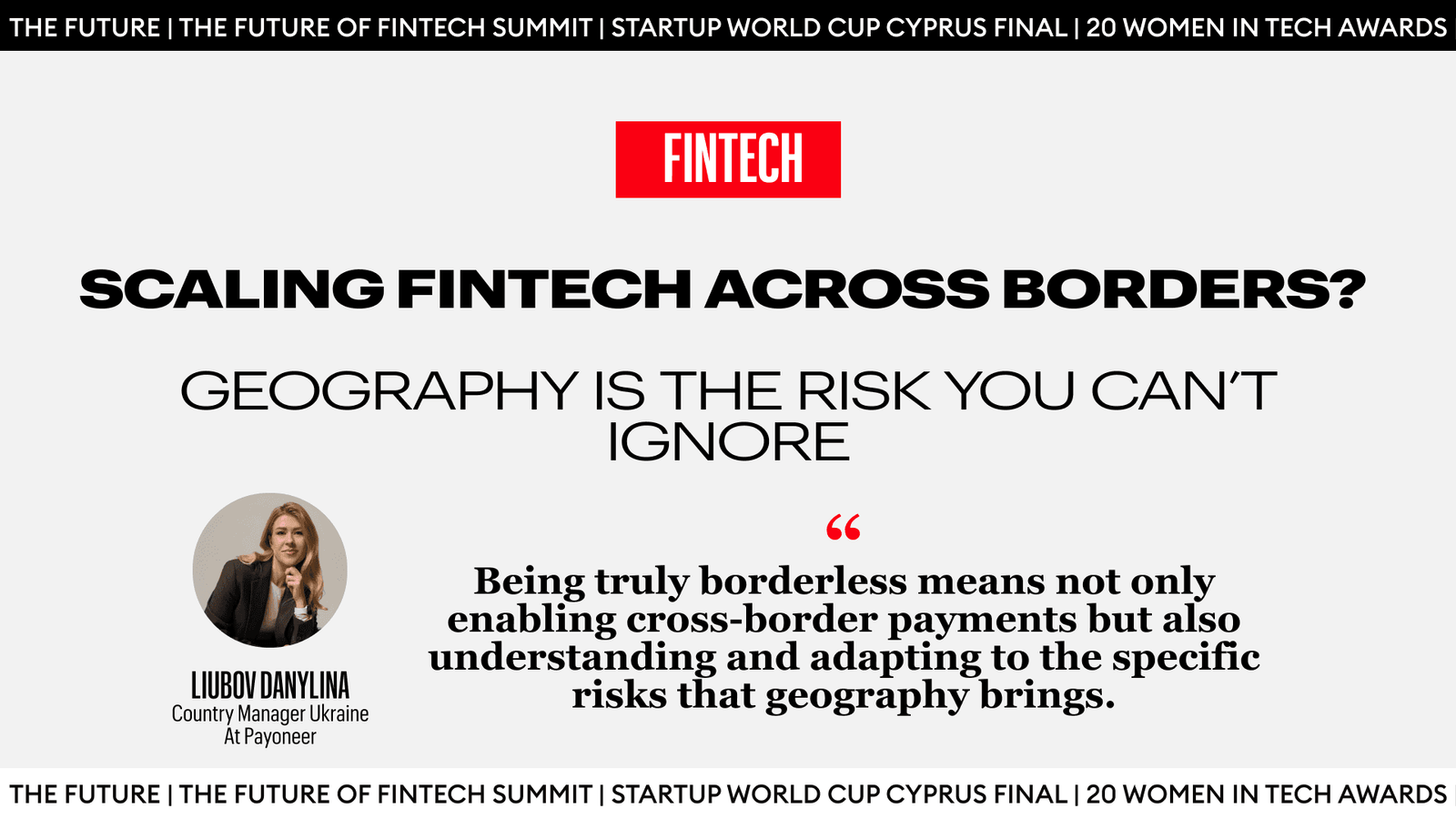

As Liubov Danylina of Payoneer put it:

“Being truly borderless means not only enabling cross-border payments but also understanding and adapting to the specific risks that geography brings.”

This article explores why fintechs can no longer afford to treat geography as incidental and how integrating it into risk planning offers more than just resilience. It’s a proactive strategy.

Environmental Risk: What Can—and Can’t—Be Outsourced

Fintech may be cloud-based, but its infrastructure is still tied to physical reality. Where a company chooses to host its servers or operate offices matters. A wrong decision can expose their infrastructure to natural disasters, from floods and wildfires, all the way to hurricanes, that no level of digital abstraction can fully mitigate.

A November 2024 study published in Risk confirms this: environmental risks tied to the location of physical assets significantly impact operational continuity, safety, ICT systems, and compliance in fintech firms. Human safety aside, data center downtime, service disruption, and insurance exposure all translate into financial risk (MDPI, 2024). These concerns are especially pressing for fintechs reliant on always-on platforms or latency-sensitive operations.

That’s why some fintechs are seeking geographic resilience by operating within “smart cities”—locations designed for sustainable infrastructure, reliable utilities, and climate adaptability. The Fintech Times (April 2025) highlights this trend toward smart-city environments as a natural buffer against system failure.

So, if extreme weather is unavoidable, the best mitigation may be choosing locations where system failure is less likely in the first place.

Regulatory Risk: Navigating Cross-Border Compliance

Few challenges expose the friction of geography in fintech more than regulation. From differing KYC requirements to evolving data sovereignty laws, what works in one country can be noncompliant, or, in some cases, even penalized, in another. For fintechs operating or expanding across borders, regulatory navigation is a strategic necessity.

Some jurisdictions offer fintech sandboxes and streamlined licensing. Others present patchwork or fast-changing frameworks where compliance hurdles multiply. “Even in neighboring countries, licensing structures, onboarding rules, and compliance expectations can vary widely—and change quickly,” said Liubov Danylina, Country Manager Ukraine at Payoneer. “Failure to anticipate those differences can lead to serious delays or operational disruptions.”

One example of navigating this legal terrain effectively is Revolut, which turned regulation into a growth lever. The UK-based fintech used regulatory sandboxes in both the UK and Lithuania to test products under real-world conditions while working closely with supervisors, streamlining its entry into new markets across Europe and beyond. This allowed Revolut to navigate the European Union’s General Data Protection Regulation (GDPR), one of the world’s most stringent data privacy laws, while preparing for jurisdiction-specific frameworks in markets like the United States.

Rather than relying on one-size-fits-all compliance strategies, Revolut localized its legal, risk, and engineering operations. It established regional teams and tasked them with interpreting and applying regional laws. These included anti-money laundering (AML) protocols in the EU and state-level regulations in the U.S. The company then went on to build internal tooling to automate regulatory monitoring. This approach helped the company adapt quickly to change while maintaining customer trust. According to DigitalDefynd (2025), these efforts were instrumental in supporting Revolut’s rapid international expansion and helped it reach a $45 billion valuation by 2024.

The takeaway here for fintechs scaling across borders is to reconsider their approach to regulation. Rather than treating it as a box to tick, regulation needs to be embedded into how fintechs scale, guiding how products are built and where they’re launched.

Infrastructure Disparities: Why Fintechs Can’t Assume Connectivity

Reliable digital infrastructure is one of fintech’s baseline assumptions but that assumption doesn’t translate across borders. In many markets, internet instability, unreliable cloud support, and legacy systems create operational risks that can compound quickly when left unaddressed.

Here’s how infrastructure limitations translate into business risk:

- Connectivity isn’t equal. While markets like the US and EU benefit from stable, high-speed networks, many emerging regions still face outages, latency, and inconsistent mobile access.

- Cybersecurity exposure varies. Poor infrastructure often goes hand-in-hand with weaker security postures, making fintechs more susceptible to fraud or breaches in lower-resourced areas.

- Digital adoption isn’t guaranteed. Even in countries with high internet penetration, rural populations or underserved urban zones may be excluded from fintech platforms due to limited device access or digital literacy.

- Operational resiliency must be localized. The same product architecture that performs well in New York may falter in Lagos without backup systems, offline capabilities, or adaptive UX.

These limitations don’t just add friction—they introduce failure points at critical moments of user interaction.

One example comes from India’s Paytm, which faced major growth bottlenecks in rural areas due to patchy and unreliable connectivity. Rather than scaling back, Paytm took the initiative to localize. By building offline payment capabilities and forging partnerships with telecom providers, Paytm added 30 million new users in areas that other platforms might have written off altogether (DigitalDefynd, 2025).

The lesson to be learned here is: fintechs must tailor infrastructure strategies to each geography. This is not just for growth, but also to prevent operational drag and reputational damage. What counts as a “minimum viable experience” in Berlin may not even function in Nairobi.

Socioeconomic Risk: Opportunity in Volatility

Emerging markets offer fintechs both a growth engine and a risk multiplier. High rates of financial exclusion, limited credit infrastructure, and economic volatility create demand, but also elevate default risk, fraud exposure, and operational hurdles.

- Market size ≠ market readiness. As Liubov Danylina of Payoneer noted, success depends less on perceived risk and more on preparation: “Fintechs can sometimes misjudge regions by focusing too much on surface-level indicators like market size or GDP, while overlooking deeper structural or cultural dynamics.”

- Credit models often fail to translate. In regions where formal credit histories are scarce or consumer behavior diverges from traditional benchmarks, imported underwriting frameworks underperform. Brex, for instance, adapted its AI-based credit assessment to emerging Southeast Asian markets, reducing default rates by 30% (DigitalDefynd, 2025).

- Local trust is earned slowly. In Gulf states, for example, digital adoption is high, but trust and relationship-building remain paramount. Fintechs may underestimate how long it takes to convert interest into partnerships.

These dynamics reveal a consistent pattern: fintechs entering high-growth but volatile markets can’t rely on scale alone. Whether it’s credit scoring, onboarding, or customer engagement, success depends on translating local realities into product and operational choices.

Fintechs that succeed in these markets do so not by pushing a global product, but by building trust locally, adapting infrastructure, and rethinking what risk actually looks like on the ground.

Strategic Implications: Turning Geographic Risk Into Competitive Advantage

Geography may introduce risk, but for fintechs that adapt strategically, it can also offer leverage.

Location influences more than compliance or connectivity. It determines how fintechs build, who they hire, how they manage data, and how quickly they can scale. The most resilient companies treat it as a design consideration, not an afterthought.

Some of the most effective strategies emerging from the field include:

- Site selection with resilience in mind. Smart cities with sustainable infrastructure can reduce exposure to environmental risks. Choosing regions with stable power grids, minimal climate-related disruption, and strong local governance is increasingly a business imperative.

- Localized compliance architecture. Companies like Revolut have shown how regulatory sandboxes and in-market compliance teams can turn friction into speed. AI-driven tools are helping, too, streamlining onboarding and monitoring regulatory change at scale.

- Cybersecurity tied to infrastructure realities. Fintechs in high-risk or high-frequency trading hubs like New York are investing heavily in real-time fraud detection and AI-based monitoring. Plaid, for instance, cut its fraud losses by 25% in 2024 by doing just that (Global Fintech Hub, 2025).

- Risk modeling tailored to regional data. Brex, operating in Southeast Asia, built its own underwriting models using alternative credit signals to compensate for sparse or inconsistent data, cutting default rates by 30% (DigitalDefynd, 2025).

- Balanced expansion. OPay grew across Africa by anchoring its model in Nigeria and expanding outward only after building strong partnerships with local banks and telecoms. The strategy: de-risk before scaling.

As Emerald Insight (2025) reports, fintechs working in underserved regions face real structural obstacles, but when they respond with targeted solutions, they drive financial inclusion and long-term growth.

The bottom line here is: geography isn’t just something to work around. For fintechs building with staying power, it’s something to build into.